RBA sets cash rate at 0.75% — Are we going to hit the Zero Lower Bound?

On the 1st of October, the Reserve Bank of Australia announced a reduction in the cash rate to a record low of 0.75 per cent in an apparent attempt to restart a stagnating economy.

The 25 basis point drop has been the third interest rate cut since May, in what appears to be a substitute to calls to increase government stimulus. The move is aimed at firming the weakening job market, boosting household spending, and lifting wage and inflation growth. However, lower rates have historically lead to an increase in housing prices, leaving many questioning the equitability of the rate cuts.

Why the cut?

As discussed in our previous article, Australia’s economy had been showing signs of a downturn. The rising rates of unemployment and underemployment have made it more difficult for the RBA to lift inflation to its target rate of 2.0%.

Households are increasingly cautious with their spending, with consumer confidence data showing a gloomy outlook from Australians.

Globally, the threat of a lasting US-China trade war and uncertainty around Brexit had sparked concerns in the financial markets. This triggered central banks around the world to continuingly cut interest rates.

What does this mean for those holding a mortgage?

Although the cash rate had been slashed to a record low of 0.75%, history suggests that only a partial cut will be passed on to borrowers. Borrowers will most likely only see a change ranging somewhere between 0.15% —0. 20%, said Canstar finance expert Steve Mickenbecker.

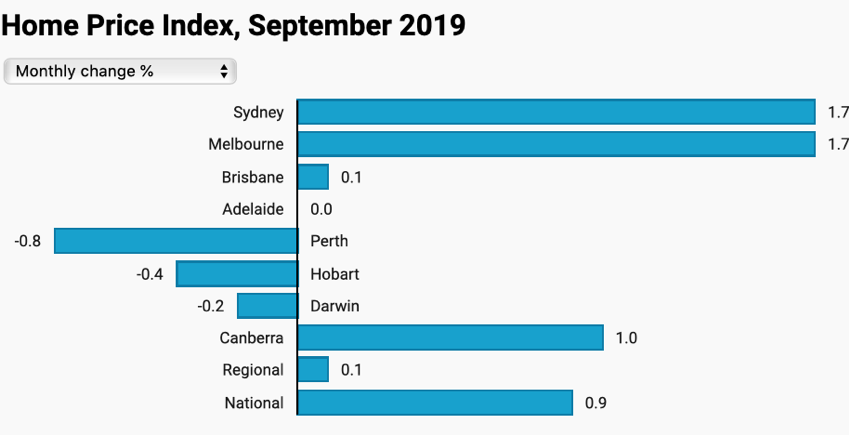

How about property prices?

Fuelled by the mid-year rate cuts, Sydney and Melbourne property prices jumped 1.7 per cent in September, following similar gains in August. However, the gains were not equally felt by other cities.

After almost two years of price dives, with housing values drop 15% in Sydney and 11% in Melbourne, prices in those cities have now rebounded, increasing 3.5 per cent in the last quarter.

According to CoreLogic Head of Research Tim Lawless, even though house values are improving, the national pricing index remains 6.7% below the October 2017 peak, indicating that buyers still have some time to take advantage of the market before values return to record high.

What does the cut means for savers?

For savers, it is not all good news, with effectively no returns now offered on big bank savings accounts, besides bonus and introductory rates.

“With the base savings rate for most online savers below 0.15% and shrinking towards zero, it is time for savers to look around the market for a better deal,” Canstar’s Steve Mickenbecker said.

Finally, what does this all mean for businesses?

Good news! Well, maybe…

It is expected that lower interest rates will promote greater consumer spending and cheaper business loans.

Whilst the current effect of the cut may be mild regarding capital costs, economists are expecting more cuts from the central bank after the RBA’s statement said a period of low rates would be needed to achieve “full employment”. This is a noticeably higher bar than the RBA’s past policy goals of “reducing unemployment”, likely signalling steady confidence in Australia’s future economic performance. This is collectively expected to translate into more realised interest savings as rates further lower, while a hopeful increase in consumer spending means a more stimulated economy.

So, what now?

Many expect a further cut in the interest rate in the upcoming months, given Australia’s spare capacity. However, with private banks controlling most of the lending in Australia, and their reluctance to pass on the rate cut, many questions the effectiveness of another rate cut.

LUCA Plus

Your all-in-one tool for better cash flow, and back-office efficiency. We are the world’s first end-to-end business transaction network for sole traders, freelancers, and small to medium sized businesses. LUCA Plus has developed accounting solutions such as secure e-invoicing, income projection, multi-channel payment options, and more to improve cash flow and manage invoicing & bills in the cloud.

Recent Comments